Sussex has been strongly advocating an active Japan equity exposure, either via hedge funds (long/short) or specialist long only managers, for a number of years now, and have been quite vocal about the opportunity in this space. This conviction was expressed early on to investors, including in past articles for The Hedge Fund Journal. The goal was to explain the rationale for the strong belief that Japan warranted an allocation on a standalone basis, irrespective of what macro views investors may hold on Japan. The stated view was that, unless investors ceased taking a simplistic, macro-based view on Japan, stopped trying to chase beta, and instead started focusing on the alpha opportunity presented by this market, they risked missing out on the real opportunity and the reason to get excited about Japan in the first place. Over the past 6 months, not a day seems to have gone by without yet another investment bank upgrading Japan to a “buy” or “overweight” rating. There has been a significant increase in investor interest as a direct result of this and corresponding asset flows into Japan (almost 2 trillion of net investment by foreigners into Japanese stocks were recorded in October alone, for example). In response to investor inquiries, Sussex has decided to provide allocators with a succinct overview of the Japanese hedge fund market, its anatomy, and thoughts on how to best approach such investments. It should be noted that, since our advocacy of investing in Japan began, many of the best managers, capable of rewarding existing investors with very attractive risk adjusted returns, have now hard closed to investors. Therefore, just as investors seem to have awoken to the hedge fund opportunity in Japan, the task of actually finding suitable hedge funds with capacity has become increasingly challenging. The following Q&A is meant to assist allocators in better understanding the market, its dynamics, and the opportunity.

Q: Why should investors consider investing in Japan in the first place, and if they decide to invest shouldn’t they just buy an ETF rather than a hedge fund?

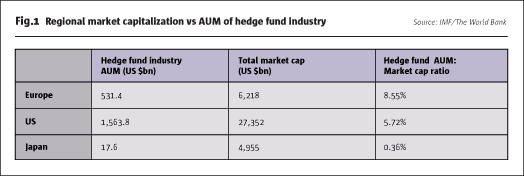

A: In our view the main reasons for investing in Japan are the inefficiencies of this market. These have been caused in part by the fact that investment banks significantly reduced the number of analysts focused on Japanese equities after the last crisis, leaving the vast majority of companies with no coverage; of the approximately 3600 listed companies in Japan, an estimated 70% have no analyst coverage, with attention focused heavily on the largest-cap stocks. In addition, the hedge fund industry in Japan has contracted considerably when compared to pre 2008 crisis levels. This means that the ratio of hedge fund assets to overall market capitalization in Japan currently only stands at approx. 0.36% (we have seen estimates as high as 1.5% but from experience feel this is too high). This compares to approximately 8.55% in Europe and 5.72% in the US.

It is easy to see from this data alone (even at the 1.5% level) that there is less “smart money” chasing the same ideas when compared to the US or Europe. This is also evidenced by ongoing conversations we have with Japanese managers. Crowded trades rarely seem to be a significant concern, and the ideas that they discuss with us are quite different from manager to manager. A correlation analysis of long/short managers in Japan (for a more complete analysis please refer to our article in the April/May 2017 issue of The Hedge Fund Journal) further supports this by showing that correlation among Japanese long/short hedge funds is generally quite low, with the majority of the 10 largest Japanese hedge funds exhibiting a correlation of below 0.5. It is also important to note that the Japanese markets are deep and liquid which means that shorting is easy and inexpensive. These market characteristics result in the additional bonus of good liquidity for hedge fund investors. This clearly points not to a top-down macro view on Japan, but to an alpha play supported by empirical data, and the 10 year outperformance of Japanese long/short equity hedge funds versus their long only equity benchmarks has been superior to that of US or global peers.

Timing markets has always been fraught with peril, except during periods of extremes such as in a clear post-crisis environment, and no matter how well-informed/market savvy an investor may be, trying to pick a top or bottom is often times a futile exercise. Sussex prefers to try and exploit market inefficiencies in order to extract continuous and more stable alpha. There are many examples of Japanese managers having, for extended periods of time, generated very attractive absolute returns, most notably in periods when the Japanese markets either were down or traded sideways.

The end result has been significant outperformance versus long only indices with a fraction of the volatility and downside. While an ETF may appear to be cheap and easy to implement, we feel that ultimately it may prove to be very costly resulting in a vastly lower long-term absolute and risk adjusted returns.

Q: How many hedge funds are there in Japan, what is the size of the industry, what strategies are available, and how many are actually still open to investment?

A: The Japanese hedge fund industry is surprisingly small given the size of both the Japanese economy (2016 GDP: approx. $4.94 trillion) and the Japanese financial markets (total market capitalization approx. $4.95 trillion). Estimates for the number of funds range from 80 to 120, managing between $18 billion and $50 billion in total assets, (depending on how broadly one defines Japanese hedge funds, ie funds managed by Japanese nationals, funds managed from Japan or abroad, funds open to foreign investors or only domestic structures etc.). Of these, approximately 30-40 are hard closed to investors, and Sussex estimates that at least half of the remaining funds have an AUM of below $100 million. In terms of strategies the industry is dominated by fundamental research-oriented long/short equity managers and most of them tend to be generalists rather than sector specialists. Those managers with a higher proportion of small and mid-cap allocations tend to hard close between $200m–$400m of assets under management in order to ensure that they stay nimble and liquid (a lesson they have learned navigating numerous crises over the past decades). There are however a few sector specialists focused on health care (hard closed), the services sector and technology, amongst others. In addition to this, there are also market neutral, event driven, relative value, arbitrage, systematic, active trading and shareholder activist funds in Japan. Shareholder activist funds tend to have a net long bias and often ask for multiyear lock up periods to match their strategy’s holding period. Our experience has generally been that net exposures range from -20% to +70%, with a majority hovering around 30%, which in our opinion also best fits the aim of generating uncorrelated returns with little beta.

Q: What are the return drivers for Japanese hedge funds? Are solid risk-adjusted opportunities mainly in the small and mid-cap space or is the opportunity broader?

A: The main driver of alpha is the fact that the market is inefficient as posited above. While it is true that there are ample opportunities in the small and mid-cap space, continued research has unearthed a number of managers which have generated very attractive returns (absolute and risk adjusted) that are either market capitalization agnostic or focused on large, or even mega cap, companies. They are able to generate these outsized returns through their bottom-up research process (referring back to the lack of analyst coverage mentioned above), concentrated portfolios of high conviction ideas, or the ability to trade the market better than peers (active trading funds or being able to better predict cycles than peers). It is also quite usual, though perhaps surprising to investors that are new to Japan, that many funds have in excess of 100 positions, and often over 200. This on the one hand speaks to the breadth of opportunities, but also has to do with their approach to risk management, which is quite conservative compared to other jurisdictions. In Sussex’s prior article it was pointed out that Japanese long short hedge funds tend to be better at capital protection than their US or European counterparts (from January 2012 to May 2015, a period in which the Japanese markets had one of the strongest rallies in recent years, Japanese long/short hedge funds had less than 1/3 of the maximum drawdown of the TOPIX index) and this greater level of diversification certainly plays a role. In addition to the key role of diversification in risk management, manager research skill in picking names has been shown to provide a superior upcapture/downcapture of market betas. We have, for example, identified concentrated, long only managers that, as a result, have been able to capture almost all of the market beta over a full market cycle but only about half the downside. The fact that Japan is a centralized country, with most companies having offices in Tokyo, is also a contributing factor, allowing managers to visit 3 or 4 companies a day, something that is much more challenging in other parts of the world where long travel distances cannibalize research time.

Q: What environment is challenging for Japanese hedge funds?

A: The response is somewhat dependent on the strategy a particular fund employs. For the many managers that have a fundamental approach to investing, periods in which there is either active intervention from the BOJ, or broad based and indiscriminate buying (or selling) from foreign investors (which often only look at Japan as a macro trade) might result in short-term losses. This is due to the distorting effect of such actions, with fundamentals being cast aside and positions (both longs and shorts) diverging from their true values as perceived by managers. In most cases though, provided risk parameters haven’t been breached and fundamentals haven’t changed, managers won’t be making significant adjustments to their positions in such circumstances, as the aforementioned distortions tend to create additional return opportunities. There have been many instances where such drawdowns were followed by periods of significant outperformance as markets began trading on fundamentals again – the beginning of October to the end of October of this year was one such period. Therefore, if one understands the return drivers and positioning of a portfolio well, these periods of underperformance can present attractive entry points, especially given the limited research coverage in Japan. Net exposures, incidentally, are often not a result of a top down view, but rather a result of opportunities managers have identified, with net exposures tending to be relatively stable even during periods of extreme inflows into Japan.

Q: What manager characteristics should investors look for in Japanese hedge funds?

A: Both pedigree and experience are always key considerations when vetting managers and perhaps more so in the case of Japan, a market that has gone through prolonged crises with often violent moves. Therefore, being able to identify managers who have not just experienced these different crises but who have managed to thrive through them is a good starting point. It is also critical for investors to understand the pedigree of a manager, and by that we mean where he/she learned to trade, as this will often be telling of trading styles going forward. Prop desks of many Japanese banks are historically very risk averse (one fund manager for example told us that when he was running a $200 million book for a local bank he was told that any losses in excess of $200,000 or 0.1% would lead to his immediate dismissal) and it is therefore not unusual for equity traders to generate returns that are more bond than equity like. We have seen many cases where fund returns were extremely and impressively stable over time, but which are so low post-fees that an absolute-return allocation is not warranted. A further point to consider is the size and hence operational infrastructure of many Japanese funds. It is not unusual to find funds that are sitting on smaller platforms (sub $500 million total AUM) and where, in effect, the manager is a “one-man band” with some shared, but quite limited, operational support. While this isn’t necessarily an issue in all cases, it is a risk that needs to be carefully analyzed, and one which may disqualify a large part of the universe of open funds for institutional investors. Further considerations are the location of the manager (preference is for Japan-based managers especially if they have a fundamental approach), the language barrier (in some cases foreign investors may be told what they may want to hear rather than what is actually going on), capacity and liquidity (funds that close at a lower AUM instead of asset gatherers are preferred), and the ability to cross-check and cross-reference individuals and information (understanding who the backers and local service providers of a particular fund are often provides important clues). A detailed understanding of corporate structures, alignment, and compensation in Japan, especially when dealing with very large firms is germane. It is not unusual for a key team member to be called away due to internal ‘job rotations’ and to be replaced with a new person from a completely different department, for managers not to be allowed to invest in their own products, or to not have their compensation tied to performance. While these may not be seen as problematic for local investors, most foreign allocators would disagree, and therefore spending time on these aspects during due diligence avoids future surprises. Sussex has also found that many of the most interesting funds are not set up to accept foreign investments or non-JPY denominated investments. Allocators may need to build a relationship with these managers first and spend time on setting up the required structures. This effort and use of resources therefore presupposes a certain minimum investment size and scale of investment program.

Q: What is Sussex’s outlook and conclusion?

A: Sussex remains bullish about the opportunities in Japan and, provided that there aren’t any sudden and significant increases in hedge fund assets or significant increases in analyst coverage of the investment universe, are convinced the alpha opportunities in Japan will continue to be significant. Should the ratios highlighted above approach levels in the US or Europe currently, then a reassessment of the proposition would be warranted. The macro-driven interest in Japan has exacerbated the difficulty in sourcing institutional quality funds with capacity. It can be challenging for foreign investors to identify the best opportunities and conduct due diligence locally, partially due to the language barrier and cultural differences (not present in the US or Europe). The opportunity is attractive enough to warrant non-Japanese investors committing the time and resources to familiarize themselves with this alpha-rich market. We strongly believe that the ingredients for alpha generation currently present, such as de minimis analyst coverage, less noise around fundamentals, and lack of long/short capital will not disappear in the near term. To us this means that a long term, active and absolute return oriented Japan allocation should be a part of most investor’s portfolios, and Japan Is likely to remain one of the most alpha rich regions for hedge fund investing for the foreseeable future.

- Explore Categories

- Commentary

- Event

- Manager Writes

- Opinion

- Profile

- Research

- Sponsored Statement

- Technical

Commentary

Issue 129

Japanese Hedge Fund Opportunities

Anatomy of the market

PATRICK GHALI, MANAGING PARTNER, AND JIM NEUMANN, PARTNER, SUSSEX PARTNERS

Originally published in the January 2018 issue