Pierre Andurand’s track record makes his strategy one of the top performers in any category – and not only within the commodities space. Stitch together the BlueGold (+241% cumulative) and Andurand Capital (+105% cumulative) track records and you arrive at annualised returns of 35.7% and total returns of 600% between February 2008 and March 2015. These returns have actually been achieved by those BlueGold investors that took the opportunity to carry forward their individual high-water marks from BlueGold to Andurand Capital, which has now fully recovered Andurand’s only losing year in eleven, 2011, and made new highs. (If the clock starts in September 2004 with his proprietary trading track record from Vitol (+380% cumulative) then total returns compound up to more than 3,200%, though no external investor has received this; data is not disclosed for his earlier proprietary trading at Goldman Sachs and Bank of America). These annualised returns in the thirties are in the same league as legends such as George Soros or Stanley Druckenmiller in their heydeys.

Triple (or quadruple) digit returns are most often seen during an extended bull market for the relevant asset class, but Andurand’s main market – oil – is down since 2008 and roughly flat since his Vitol days. Andurand is a trader who has consistently captured both directional and relative value moves, in both directions, mainly in energy, but also now in currencies and metals. But, as Table 1 shows, he has done this with no meaningful correlation to hedge funds in general, commodities or equities.

Brent Crude and West Texas Intermediate

Andurand’s profits from accurately calling oil price crashes in late 2008 and late 2014 naturally grab the most headlines, but he does not rely exclusively on directional moves in oil. Between 2011 and late 2014 oil prices were trapped in a narrow trading range that might have encouraged some traders to sell volatility – but Andurand, who only buys options, sought opportunity in relative value. Andurand has at his disposal a wide repertoire of relative value trades, including calendar spreads (which have come to the fore in 2015), crack spreads between raw and refined products, and spreads between different energy markets, but it was geographic spreads that accounted for nearly all of his 2013 return. In 2013 the wide price gap between Brent Crude and West Texas Intermediate, the two leading and liquid global futures contracts, caught his attention. The potential game changer was that new pipelines between Cushing, Oklahoma, and the Gulf Coast could collapse the spread between WTI and the Gulf Coast benchmark, Louisiana Light Sweet (LLS), which, throughout most of recent history, has been closely linked to Brent Crude prices. Andurand’s thesis, which dissented from the sell-side consensus, played out with remarkable speed as the spread compressed from $17 to zero in a matter of months – and there was even a fleeting opportunity for Andurand to take off 40% of the position at an ever so slightly positive spread.

That Andurand can be as disciplined about locking in profits as he is about cutting losses proved to be crucial in 2013, as the spread blew back out even faster than it had compressed, coming round full circle to end the year roughly where it had started. The new departure in late 2013 was that LLS temporarily decoupled from Brent crude, dropping to a discount of $16 that was $14 more than ever before. Suddenly LLS rather than Cushing was dictating the Brent/WTI spread. “Two years later I still do not understand what was driving this move,” says Andurand, and indeed today LLS is back to moving in lockstep with Brent. But Andurand and his risk management policies are respectful of markets, so he eliminated his remaining exposure to the spread trade after a 30% pullback, thus avoiding the next 70% of the reversal. So in 2013 Andurand captured more or less 100% of the re-convergence between Brent and WTI, while avoiding most of the pullback.

Oil price crashes

In his best ever year, 2008, Andurand’s BlueGold did even better and captured both the parabolic apex of the oil bull run and its precipitous spike down. Once again in 2014 the sharpest fall in oil since 2008 was Andurand’s best trade, but for the first eight months of the year the open-minded Andurand had in fact maintained a neutral to bullish bias. “We thought the market would remain balanced as US shale production growth had, coincidentally, been exactly offset by supply disruptions from North Africa and the Middle East for some years,” he says. Given this equilibrium, Andurand had thought that geopolitical risks could cause higher prices so he did briefly attempt some long positions during 2014. But in September 2014 Andurand began to change his mind. Seldom does Andurand immediately cut and reverse from long to short, as he tends to spend a few weeks pausing for thought with no position and is quite content to stand aside from the market whilst mulling over the data and plotting his next move.

The salient data points that helped reverse positioning in September 2014 included the IEA confirming oil demand growth had slowed to 700,000 barrels per day (bpd), from the previous forecast of 1.4 million; Iran and particularly Libya ramping up production; and non-OPEC supply rising somewhat faster than expected. Andurand started going short in September, but only increased to a maximum position size after the November OPEC meeting refrained from cutting production – something he had viewed as a likely prospect. He had argued that if OPEC had been planning a drastic cut then an emergency (rather than a planned) meeting would havebeen scheduled, and Saudi Arabia, Kuwait and the Emirates would probably have cut production before the meeting. Andurand also reflects on how the OPEC cartel has been disintegrating for years, as there are no longer quotas per country, with Saudi Arabia, Kuwait and the Emirates the only members likely to cut. Andurand surmises that OPEC decided not to cut at all because “with non-OPEC supply growth alone structurally greater than global demand growth at $100+ oil, this was a war that they could not win.” When the consensus view of a cut was confounded, Andurand moved in for the jugular and stepped up to full position size.

At the time of writing at the end of April 2015, Andurand is once again contrarian in being sceptical about the popular view that lower oil prices will choke off shale production. He does see scope for some near-term dip in US production, but longer-term he points out that efficiency gains are relentlessly driving down costs. “Two years ago in the Permian basin you needed $95 oil for a 15% Internal Rate of Return (IRR): now the figure is $50 and maybe it will be 35 later on.” The same dynamics have been seen in natural gas, where Andurand recalls how in 2008 lower rig counts led pundits to predict lower production. In the event, Andurand claims production went up as marginal costs plunged from 7.50 to 2.50. “Rigs and fracking are becoming more efficient,” summarises Andurand. Just as the shale companies are drilling more effectively, so Andurand is digging into granular data from drilling consultants who enumerate costs down to the level of individual wells and basins.

This data leads Andurand to postulate that US production is near its peak and about to decline by about 400,000 barrels per day in the next six months before increasing again – but he notes OPEC production is rising with Saudi up to 10.3 from 9.7 million bpd, Libya recovering to 600,000 from 200,000 and Iran potentially adding 800,000 within a year if sanctions are lifted. Andurand refutes several other fears over supply with very clear views. He argues that China’s loans might keep Venezuela pumping oil even if it does default; Nigeria’s new president simply needs to pay off terrorists; and if the Yemen situation worsens a closure of the Yemen strait would simply divert oil around the Cape route, adding a dollar or so to costs, but with the strait probably reopened within days by Egypt’s Navy. All of this means that Andurand envisages an ocean of oil inventories testing maximum storage capacity some time in 2015 or 2016, and thinks that a glut of supply could lead to new lows in the oil price – but more importantly this could steepen the contango.

But Andurand trades around his core views. In early 2015 Andurand covered his short with near-perfect timing, sidestepping the sharp bounce in Brent crude from $44 to $64. He has also been tactical in rebalancing the euro position, taking profits after dollar rallies and then adding again on dollar dips. Andurand’s perspective on the US dollar is unusual in being informed by oil, as well as by a continuing dialogue with former colleague Stephen Jen of SLJ Macro Partners, which sits in the same Knightsbridge office building (and was profiled by The Hedge Fund Journal in 2013). Jen has long been a cheerleader for the dollar, whereas Andurand thought the oil drop was the catalyst for the sharp move up. There is a technical monetary policy reason for why oil helps to explain the dollar rally. Explains Andurand, “The Bank of Japan and ECB both look at headline inflation, including energy and food, whereas the Fed looks at core inflation excluding oil prices.” This clearly means that lower oil prices give the BOJ and ECB more impetus to expand or embark on QE programmes, while lower oil would not remove the need for the Fed to act in response to rising prices. Also, a weaker oil price leads to a smaller current account deficit for the US, and leads to less petrodollars recycling, helping to strengthen the US dollar.

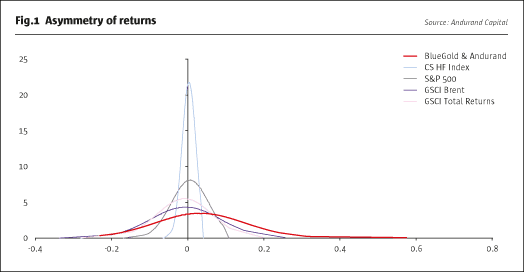

Asymmetry and risk management

Occasionally weather can inspire trades. The big freeze in the US in early 2014 led Andurand to buy natural gas and heating oil, but he did so partly because “the optionality is cheap with inventories low, so the worst case was to lose small and the best case was to make lots.” Andurand is always seeking hugely asymmetric pay-off profiles where he could risk one to make 10, 20 or even 40. “My 3.5 to one upside to downside ratio is key, and drawdowns have to be manageable, and not impact my confidence and my investors’ confidence,” he says. Fig.1 shows the extraordinary asymmetry of Andurand’s return profile.

Constructing trades with an asymmetric risk/reward profile is the foundation of the investment philosophy, but risk management at Andurand Capital is subject to tighter limits and risk reduction rules than applied at BlueGold. Net leverage has been much lower and maximum Value at Risk (VaR) is down from 5.5% to 2.25% (though the average has been 1.3% in 2014) with a tiered risk reduction ladder requiring staggered cuts in VaR at drawdowns of 3%, 8%, and 11%. “At down 15% we take a break of at least two weeks to ensure that we are not emotionally attached to positions,” says Andurand. This was tested in December 2013, when the traders did indeed take a two-week holiday. In a sign of the growing power of fund directors, the independent fund directors of Andurand Capital are empowered to issue trade instructions if any breaches of risk limits have not been remedied, but there has been no need to resort to this.

Andurand’s nickel trade shows how losses were cut when the idea turned out to be wrong. The catalyst for going long of nickel had been the ban on Indonesian exports, and initially prices did start rising before being overwhelmed by weaker China demand and higher Philippine exports. A small position was cut when the price began to reverse.

Career evolution

In all of these trades Andurand is pulling together the strands of knowledge from his five corporate lives as an energy trader. “Over 15 years I have gotten better and better at looking at things,” pronounces Andurand.

Each stage of Andurand’s career brought new lessons. He studied applied maths and started as an energy options trader at Goldman Sachs, which taught him how owning options could generate highly asymmetric pay-offs; Andurand does not short options. In Singapore, Andurand traded less liquid markets, and this forced him to analyse the market in more depth. His time at Bank of America taught him that overconfidence was the danger after a winning streak, and that discipline in cutting losses was important. His experience in investment banks helped him understand how corporate hedging flows create opportunities, and how they impact the forward curves and the relationships between different oil products. The third proprietary trading role at Vitol taught him further about physical markets. Over the years his supply and demand models got more precise, and his experience in running hedge funds helped him overlay a macro outlook on top of this.

Each of Andurand’s employers headhunted him, generally offering more responsibility, bigger profit shares, and a partnership in the case of Vitol. But even this, which gave him participation in Vitol’s corporate profits as well as his own P&L, was not enough to satisfy the ambitious Andurand. “I wanted to manage more money elsewhere and thought I could reproduce a great information flow,” he recalls, and BlueGold, which launched in February 2008, did indeed have peak assets of $2.4 billion.

BlueGold still had$1 billion of capital at the start of 2012, so clearly did not return capital to investors in May 2012 due to redemptions. It closed down to resolve a difference of opinion between majority owner Pierre Andurand and minority owner CEO Dennis Crema, who was focused on non-trading activity. Crema, who is about 20 years older than Andurand, has effectively retired. But 10 of Andurand’s 14 staff were also colleagues at BlueGold, showing the team’s cohesion and loyalty.

Inefficient markets

Some commodity trading funds claim to obtain informational advantages from their related party commodity businesses, but Andurand’s trades in his funds have all been based on public information. He finds that far more information is now publicly available than was the case 10 years ago, for anyone who is prepared to spend money on data that can even include real-time pipeline flows. With information quality improving, why might inefficiencies persist? The argument that hedgers can create opportunities for speculators is not new, and was formalised in Keynes’ 1930 hedging pressure hypothesis, but this could still be very relevant today. In the Brent/WTI case, Andurand reckons heavy hedging by US shale producers helped to keep WTI cheaper than Brent. Another reason why more information need not make markets more efficient is that Andurand finds many energy traders are non-specialists who may not have a deep enough understanding to interpret the data.

This year Andurand is in short mode, but he admits that his positioning could change at any time if the facts change. Longer-term, his outlook is more sanguine. “Although oil demand growth is less than world GDP growth due to efficiency gains and alternative energy sources, it will still be a challenge for supply to keep pace with demand,” he foresees. Thinking well beyond current portfolio positioning, Andurand is mapping out long-term scenarios for various oil provinces. “High-cost Arctic and Greenland projects could be cancelled and delayed, planting the seeds for the next bull run.” Sanctions in Russia could take effect in very specific ways. Unlike Iran, Russia is not prevented from selling its oil. “The problem is that they may not get access to new technology that they need to exploit shale wells and drill new fields that require western technology.” So Andurand reckons that if sanctions continue, Russia will eventually have a lower production. Europe is also very unlikely to see a shale boom without very much higher oil prices.

Not all of the former BlueGold investors have invested in the Andurand Capital fund, but many have, including pension funds, insurance companies, family offices and funds of funds. Investors are 70% US-based and head of marketing, Sara Corsaro, thinks, “Americans are more sophisticated, understand commodities better, and have sometimes made fortunes from the energy industry,” and indeed some partners of leading commodity trading firms are invested in the fund. Managed accounts or funds of one can be offered, and investors can dial up or down to different risk targets. Capacity is estimated at $1.5 billion, far less than the $2.4 billion peak assets run at BlueGold, where risk was also three times the level that applies at Andurand, and where equities were traded – they are not now. Although the capacity target is lower, Andurand finds that liquidity in his futures markets has not been much impacted by banks withdrawing from commodity trading. Numerous commodity hedge funds have also closed their doors in recent years, which may mean there is even less competition for Andurand. One thing is clear: he is still living and breathing energy markets and relishing their dynamism and volatility.

- Explore Categories

- Commentary

- Event

- Manager Writes

- Opinion

- Profile

- Research

- Sponsored Statement

- Technical