Akin: The Corporate Transparency Act’s Impact on Private Fund Managers

Immediate planning needed

Akin

Originally published on 07 January 2024

Starting on January 1, 2024, entities that are organized in the United States or are registered to do business in the United States will generally be required to disclose to the Financial Crimes Enforcement Network (an instrumentality of the U.S. Treasury (FinCEN)) the identities of individuals:

- Who directly or indirectly exercise substantial control over them, or

- Who own or control at least 25% of their ownership interests.

This requirement is imposed by the Corporate Transparency Act (CTA), a U.S. law designed to combat money laundering, and FinCEN’s Beneficial Ownership Information Reporting Rule (the BOIR Rule, and, together with the CTA, the CTA Regime).

There are numerous exemptions to this new FinCEN reporting regime, some of which were designed to provide relief for the investment management industry, but a significant degree of uncertainty over the scope of the exemptions still exists. Private fund managers, commodity trading advisers, and commodity pool operators should consult with counsel to determine whether an exemption will apply to their management company structures and—separately—to their fund structures.

While every situation will require a bespoke analysis, some points and guidelines for beginning the preparation for a discussion with counsel are set forth below. Additional FinCEN guidance is likely pending. We are monitoring the release of any such guidance on an ongoing basis.

While these kinds of registries have existed in other countries for some time, this is new for the United States. As this begins to filter into the mainstream business world, there may be civil liberties and other concerns raised.

Brian T. Daly, Akin Gump

General Obligations

Q: Who is required to report under the CTA Regime?

The CTA Regime requires domestic and foreign “Reporting Companies” to report beneficial ownership and certain other information, unless the Reporting Company qualifies for an exemption.

A domestic Reporting Company is a corporation, limited liability company, or other entity created by the filing of a document with a secretary of state or similar office under the law of a U.S. state (or an Indian tribe).

A foreign Reporting Company is a corporation, limited liability company or other entity formed under the law of a foreign country and registered to do business in the United States by the filing of a document with a secretary of state or similar office.

Note that:

- Entities that are created under U.S. state law, but not through a filing, such as a general partnerships and certain trusts, are not domestic Reporting Companies.

- Foreign entities formed without a filing under their local laws become Reporting Companies when they register to do business in the United States.

Q: What information needs to be reported?

Initial reports to FinCEN by a Reporting Company must include:

- The company’s legal and trade names;

- The current address of its principal or primary place of business;

- Its jurisdiction of formation; and

- Its Internal Revenue Service Taxpayer Identification Number.

Initial reports must also identify each “Beneficial Owner,” i.e., any individual who, directly or indirectly, either exercises substantial control over a Reporting Company or owns or controls at least 25% of the ownership interests of a Reporting Company1 and provide that individual’s legal name, date of birth, current address and an identification document (e.g., passport).

For a Reporting Company created or registered after January 1, 2024, similar information on the Reporting Company’s “Company Applicant” must also be provided. (A “Company Applicant” is an individual who, in the case of a domestic Reporting Company, directly files the document that creates or registers the company to do business.)

Q: Are there amendment/updating requirements?

Once an initial report is filed, Reporting Companies do not have annual filing requirements. However, the CTA requires the filing of updated or corrected reports if necessary. Specifically, Reporting Companies are required to file an updated report in the event that there is any change with respect to required information previously submitted to FinCEN concerning the Reporting Company or its Beneficial Owners within 30 calendar days of the change. However, changes in information concerning a Reporting Company’s Company Applicant do not need to be updated.

A Reporting Company also must file a corrected report in the event that information submitted to FinCEN was inaccurate when filed and remains inaccurate. Corrected reports must be submitted within 30 calendar days of the date on which the Reporting Company became aware or the inaccuracy or had reason to be aware of the inaccuracy.

Manager-Focused Questions

Q: Are registered investments advisers (RIAs) exempt?

The CTA Regime provides an express exemption from the reporting obligations for investment advisers registered as such with the Securities and Exchange Commission (SEC). This is good news for the industry. However, the exemption only applies to the RIA itself, so “upstream” entities that directly or indirectly own interests in the RIA may be outside of the scope of the exemption (and thus within the FinCEN reporting regime).

While there is no express guidance on this, so-called “relying advisers,” i.e., entities that register as investment advisers by means of a Schedule R on a filing adviser’s Form ADV, should come within the RIA exemption, as relying advisers are registered with the SEC through the use of the “filing adviser’s” Form ADV.

Q: Are exempt reporting advisers, such as private fund advisers and venture capital fund advisers, exempt?

The two types of exempt reporting advisers are treated differently under the CTA Regime. A “private fund adviser” that is exempt from registration pursuant to Rule 203(m)-1 under the Investment Advisers Act of 1940, as amended (the Advisers Act),2 is not “registered” with the SEC and, therefore, is not covered by the above exemption. If a private fund adviser is a Reporting Company because it is formed pursuant to a filing under domestic law or registered to do business in the United States, it would be required to report under the CTA Regime. Foreign private fund advisers that are not registered to do business in the United States would not be required to report.

A “venture capital fund adviser,” as defined in Rule 203(l)-1 under the Advisers Act, is, however, specifically exempted from reporting under the CTA Regime so long as it files the required Form ADV with the SEC that includes information about the control persons of the venture capital fund adviser.

Q: Are foreign private advisers exempt?

In most cases, “foreign private advisers”3 should be outside of the reporting regime, as they are presumably not organized under the laws of a U.S. jurisdiction and are not registered to do business in the United States.

Q: Are commodity pool operators and commodity trading advisors exempt?

Commodity pool operators (CPO) or commodity trading advisors that are registered with the U.S. Commodity Futures Trading Commission (CTFC) are exempt from reporting under the CTA Regime. CPOs exempt under CFTC Regulation 4.13 would not be exempt unless some other exemption applies.4 CPOs relying on CFTC Regulation 4.7 are registered with the CFTC,5 so they would be exempt from reporting under the CTA Regime. As with RIAs, however, unregistered “upstream” entities are outside of the scope of the exemption.

Q: Are entities that were created to serve as general partner or managing members of private funds exempt?

These types of entities, assuming they are otherwise Reporting Companies, are not expressly exempt from reporting.

However, the SEC has taken the position that, although the general partner or managing member would technically be an investment adviser under the Advisers Act, a separate special purpose vehicle that was formed for the purpose of serving as a general partner or managing member of a fund and has no officers, employees or other purposes acting on its behalf other than officers, directors or employees of the registered investment adviser would “look to and essentially rely upon the investment adviser’s registration with the SEC in not registering itself,”6 which could provide the rationale for a CTA Regime exemption (although there is no clarity on this yet). As with RIAs, the upstream owners of these types of entities are outside of any argument in favor of the application of the RIA exemption.

For foreign funds, we are expecting most entities to be out of scope. But with so many managers having US-based affiliates, we expect to see more foreign managers pulled into the reporting regime.

Nnedinma C. Ifudu Nweke, Akin Gump

Fund-Focused Questions

Q: Are private funds exempt?

There is a “pooled investment vehicle” exemption from the CTA Regime for a domestic Reporting Company that qualifies as a pooled investment vehicle and that is operated or advised by a registered investment adviser, venture capital fund adviser, broker or dealer, credit union or bank. A pooled investment vehicle is defined as:

- A private fund (i.e., a fund that would be required to register as an investment company but for the exclusion provided in Section 3(c)(1) or 3(c)(7) of the Investment Company Act of 1940) that is “identified by its legal name by the applicable investment adviser in its Form ADV (or successor form) filed with the SEC or will be so identified in the next annual updating amendment to Form ADV.”

- An investment company, as defined in Section 3(a) of the Investment Company Act of 1940.

Q: Are non-U.S. funds exempt?

Non-U.S. funds are out of scope of the CTA Regime unless they are registered to do business in a U.S. state. If a non-U.S. fund is captured (i.e., it is a foreign Reporting Company) then it cannot rely on the pooled investment vehicle exemption, but a limited reporting requirement generally applies.

To the extent that a non-U.S. fund has granted a U.S. investor the ability to have disputes adjudicated in a U.S. state or territory, coverage and compliance with the CTA Regime should be discussed with counsel.

Q: What about SPVs, trading vehicles, holding companies, co-investment vehicles, carry vehicles, etc. in the fund structures? What about funds-of-one?

There is still considerable uncertainty about whether these types of vehicles are in scope. Managers advising or preparing to launch these kinds of structures should discuss CTA compliance with counsel based on the specific circumstances.

Q: Are commodity pools exempt?

Many commodity pools are not private funds because they would not be an investment company but for Section 3(c)(1) or 3(c)(7). Instead, they rely on the SEC staff no-action letter guidance that a commodity pool, depending on its mix of assets, is primarily engaged in a business other than investing or reinvesting in securities. Also, a commodity trading advisor may determine not to register as an investment adviser if it is predominantly in the business of providing advice regarding commodity interests. Commodity pools that are not also private funds or that are operated or advised by a person that is not a registered investment adviser, venture capital fund adviser, broker, federal credit union or bank would be required to report under the CTA Regime.7

Q: What about a Fund board?

Individual directors may be included as Beneficial Owners in a report by a fund that is a non-exempt Reporting Company, but the board of directors itself will generally not be considered to be a “Reporting Company.” A company that acts as a director would have to assess coverage and whether any exemption applies.

Effectiveness and Timing

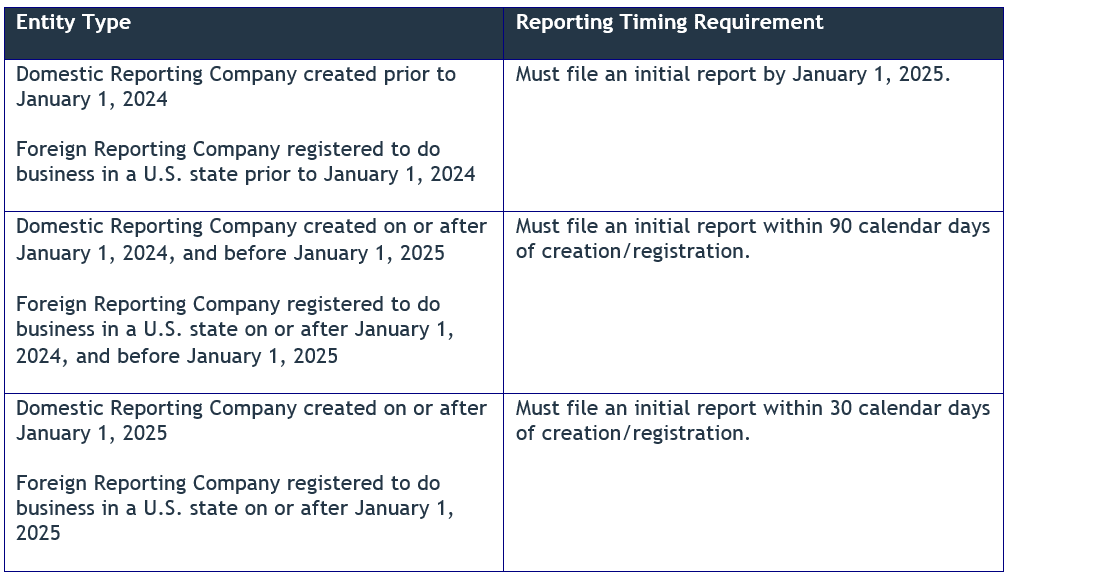

Q: When am I required to report?

The below table describes the applicable reporting deadlines for different Reporting Companies, depending on when the Reporting Company is/was established and assuming no exemption applies.

Companies should review the CTA and the BOIR Rule carefully to determine whether reporting requirements apply. For entities formed on or after January 1, 2024, but before January 1, 2025, the above regime will, unless an exemption applies, require a filing within 90 days of formation. In other words, CTA compliance needs to be part of the formation considerations for any manager client or other fund entity created in the new year.

Many open questions remain concerning implementation of the BOIR Rule and FinCEN continues to issue guidance in the form of Frequently Asked Questions. We continue to monitor developments in this space.

Footnotes

- Note that the definition “beneficial owner” is contrary to ordinary parlance and includes a person that owns or controls 25% of the ownership interests of an entity but also certain other controlling persons. Certain individuals and creditors may be excluded from the reporting regime. Ownership is calculated by reference to capital and profit interests in an entity calculated as a percentage of outstanding capital and profits interests, and options treated as if they were exercised. For corporate entities, the 25% ownership is determined by reference to the greater of the percentage of voting and value of the stock owned.

- A “private fund adviser” with a principal place of business in the United States is an investment adviser that only advises private funds and has less than $150 million in regulatory assets under management. A “private fund adviser” with a principal place of business outside the United States is an investment adviser whose only U.S. clients are private funds. If the foreign private fund adviser has a U.S. place of business, all of its assets managed from the U.S. place of business must relate to private funds and the total value of those assets must not exceed $150 million.

- A “foreign private adviser” is defined under Section 202(a)(30) of the Advisers Act and Rule 202(a)(30)-1 thereunder as an investment adviser without a place of business in the United States, with fewer than 15 U.S. clients or investors in a private fund and with less than $25 million in regulatory assets under management related to those U.S. clients or investors.

- CFTC Regulation provides exemptions from registration for commodity pool operators managing funds with de minimis exposure to commodity interests and to family office commodity pools.

- CFTC Regulation 4.7, among other things, provides an exemption from certain disclosure, reporting and recordkeeping obligations for commodity pool operators to pools with qualified eligible person investors.

- SEC No-Action Letter, American Bar Association, Subcommittee on Private Investment Entities (pub. avail. Dec. 8, 2005) available here and SEC No-Action Letter, American Bar Association, Business Law Section (pub. avail. January 18, 2012) available here.

- See National Futures Association Notice to Members I-23-23 (Dec. 5, 2023) available here.

- Explore Categories

- Commentary

- Event

- Manager Writes

- Opinion

- Profile

- Research

- Sponsored Statement

- Technical